Certified With

Sign in

Check your credit score instantly with Ruloans, India’s leading loan Distribution Company. Enjoy a seamless experience as you access your credit score for free and get a detailed credit report. Whether you’re exploring loans, insurance, or tracking your financial health, Ruloans is your trusted partner on the path to financial stability and success.

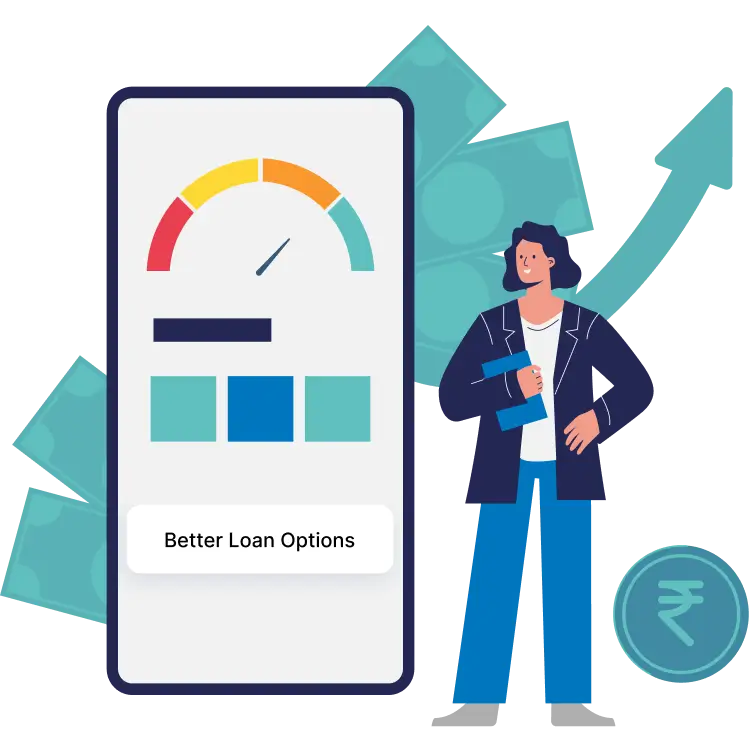

A credit score represents your creditworthiness, calculated from your credit history and financial behaviour. Ranging from 300 to 900, a higher credit score signals better credit health. Financial institutions use this score to assess lending risk. A good credit score can unlock favourable interest rates and loan terms, while a lower score may result in higher interest or loan rejections.

Regularly checking your credit score allows you to monitor your financial standing, catch any inaccuracies, and take steps to improve your score if needed. With convenient online options, staying informed is simpler than ever—you can check your credit score online with just a few clicks.

In India, the credit score ranges from 300-900 and is divided into the following categories:

Check Your Credit Score for Free with Ruloans. Follow these simple steps:

Go to Check Credit Score : Visit Ruloans website and go to ‘Credit Score’.

Sign in with Mobile Number : Enter your mobile number to sign in.

Fill out the Form : Provide your details, including your PAN number.

Get Your Score : View your Credit score instantly for free.

To monitor your credit health, you can check Credit Score online for free with Ruloans.com. With our Free Credit Score option, you can view your Credit Score report free, providing a comprehensive look at your credit profile. For a smooth experience, try our Credit Score check online and explore the advantages of online Credit Score options.

Higher chances of loan approvals from banks and financial institutions.

Access to loans at more competitive interest rates.

Managing your Credit Score is effortless with Ruloans by your side. Offering free Credit Score Checks and expert advice, Ruloans helps you monitor, manage, and improve your credit score effectively. Whether you're seeking loan products, mutual funds, or insurance, our extensive network of 275+ private banks, PSU banks, NBFCs, and financial companies ensures you get the best options tailored to your needs. With Ruloans, you not only access financial solutions but also gain the tools to build a stronger credit profile. Empower your financial future with Ruloans the partner you can trust for smarter financial decisions!

To boost your credit score, consider the following strategies:

View More

A credit score is a 3-digit number (between 300 to 900) calculated by the credit bureau using the credit history of the individual.

Banks and NBFCs (Non-Banking Financial Companies) have to share the credit history of their customers with all four credit Bureaus.

The credit history of an individual consists of credit amounts, lender names, loan and credit card limits, loan EMI and credit card bill payment records, any default on a credit card account, personal details, etc.

This may happen due to the following reasons:

You can build your credit score in 4 steps:

A credit report is a statement of all the loans and credit card history of an individual reported to a credit agency by lenders – Banks & NBFCs. Credit card history is data that has all the information about the current credit status such as credit card payments, loans, etc.

Having a good credit history gives you the benefit of creditworthiness with helps you to avail loans seamlessly.

Following are the prominent factors you must consider to manage a good credit score: