Certified With

Sign in

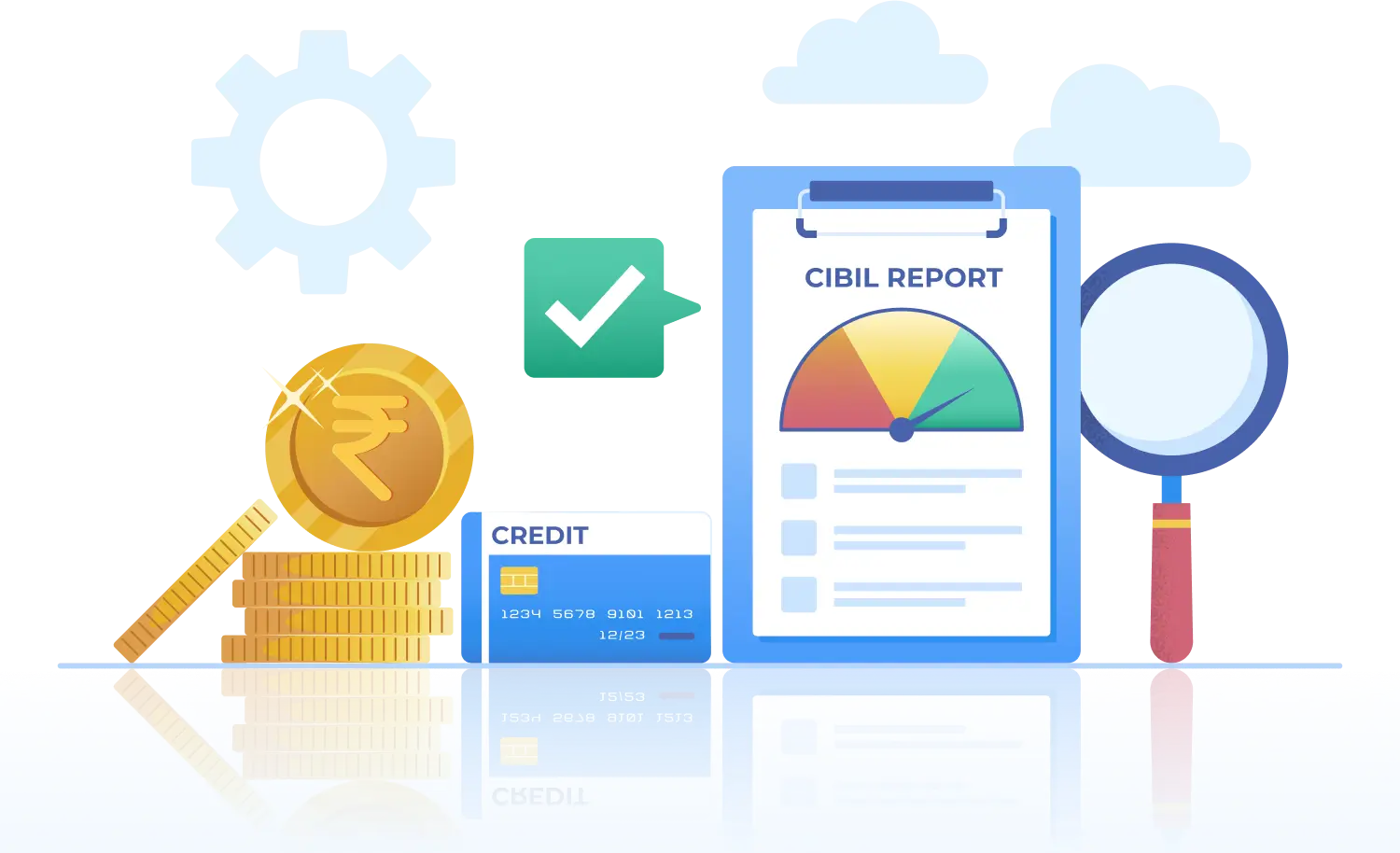

Instantly check your CIBIL score with Ruloans, India’s leading loan distribution company. Enjoy a seamless experience as you access your credit score for free and get a detailed credit report. Whether you’re exploring loans, insurance, or tracking your financial health, Ruloans is your trusted partner on the path to financial stability and success.

A CIBIL score represents your creditworthiness, calculated from your credit history and financial behavior. Ranging from 300 to 900, a higher CIBIL score signals better credit health. Financial institutions use this score to assess lending risk. A good CIBIL score can unlock favorable interest rates and loan terms, while a lower score may result in higher interest or loan rejections.

Regularly checking your CIBIL score allows you to monitor your financial standing, catch any inaccuracies, and take steps to improve your score if needed. With convenient CIBIL score check online options, staying informed is simpler than ever you can get your CIBIL score online with just a few clicks.

In India, the CIBIL Score ranges from 300-900 and is further divided into several categories:

Check Your CIBIL for Free with Ruloans. Follow these simple steps:

Go to Check CIBIL Score : Visit Ruloans website and go to ‘Check CIBIL Score.

Sign in with Mobile Number : Enter your mobile number to sign in.

Fill out the Form : Enter your details, including your PAN number.

Get Your Score : View your CIBIL score instantly for free.

To monitor your credit health, you can check CIBIL score online for free with Ruloans.com. With our Free CIBIL Score option, you can view your CIBIL report free, providing a comprehensive look at your credit profile. For a smooth experience, try our CIBIL check online and explore the advantages of online CIBIL score options.

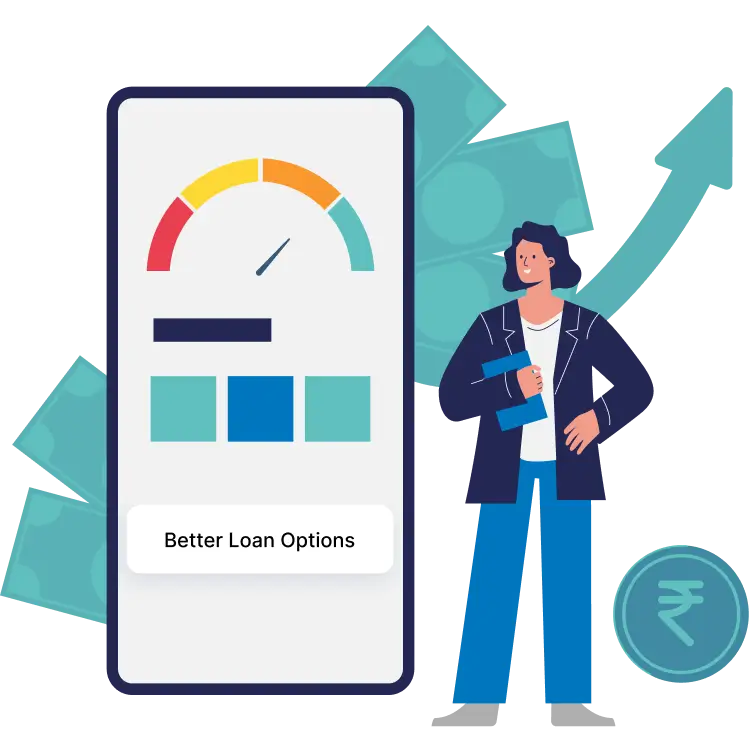

Higher chances of loan approvals from banks and financial institutions.

Access to loans at more competitive interest rates.

Managing your CIBIL score is effortless with Ruloans by your side. Offering free CIBIL Score Checks and expert advice, Ruloans helps you monitor, manage, and improve your credit score effectively. Whether you're seeking loan products, mutual funds, or insurance, our extensive network of 275+ private banks, PSU banks, NBFCs, and financial companies ensures you get the best options tailored to your needs. With Ruloans, you not only access financial solutions but also gain the tools to build a stronger credit profile. Empower your financial future with Ruloans the partner you can trust for smarter financial decisions!

To boost your CIBIL Score, Consider the following strategies:

View Less

A CIBIL score is a three-digit number that represents your creditworthiness based on your borrowing and repayment history.

It typically ranges from 300 to 900 and is one of the most important credit scores for loans.

Lenders check your CIBIL score before approving any loan or credit card to assess whether you are a low-risk borrower. A higher CIBIL score increases your chances of getting loans at better interest rates.

The maximum CIBIL score is 900, which represents the highest level of creditworthiness.

If you’re wondering how CIBIL score is calculated, it is based on several important credit score factors.

Yes, clearing your outstanding dues and completing a loan closure can improve CIBIL score over time. When you repay your loan in full, it shows lenders that you are financially responsible, which positively impacts your credit profile. However, the loan closure effect on credit score may take a few weeks to reflect in your CIBIL report as it depends on when the lender updates the credit bureau.

Yes, credit card late payment CIBIL score impact is significant.

Even a single missed or delayed payment can negatively affect your score, as repayment history is one of the most crucial factors in CIBIL’s calculation.

Consistently paying EMIs and credit card bills after the due date lowers your score, reduces your creditworthiness, and makes it harder to qualify for loans or new credit cards in the future. To protect your score, always pay your bills on time.

If you’re wondering how to improve CIBIL score, the key lies in disciplined financial management. Always pay your EMIs and credit card bills on or before the due date, and try to keep your credit utilization ratio below 30%. Avoid applying for multiple loans or credit cards within a short period, as too many inquiries can lower your score.

Maintaining a balanced mix of secured and unsecured credit also plays an important role. By following these practices consistently, you can gradually boost credit score and increase your chances of getting loans approved with better interest rates and favorable terms

No, checking your own CIBIL score does not negatively affect it. In fact, you can check free CIBIL score online anytime to stay updated on your credit health.

These are considered “soft inquiries” and do not lower your score, unlike lender-initiated “hard inquiries.” Regular monitoring enables you to identify errors and take corrective steps promptly.

You can do a free CIBIL score check online through trusted financial distribution platforms like Ruloans.

With just a few basic details, you can instantly check CIBIL score for loan eligibility without affecting your credit score.

This helps you understand your credit health before applying for a personal loan, home loan, or credit card, increasing your chances of quick approval.

There are several important factors affecting CIBIL score. These include your repayment history, credit utilization ratio, length of credit history, types of credit (secured and unsecured), and the number of recent credit inquiries.

Timely payment of EMIs and credit card bills, keeping credit usage below 30%, and maintaining a long and balanced credit history can positively influence your score.

On the other hand, late payments, defaults, or applying for too much credit at once can reduce it. By managing these factors affecting CIBIL score, you can build and maintain a strong credit profile.

A CIBIL score and report are related but serve different purposes. Your CIBIL score is a three-digit numeric summary (ranging from 300 to 900) that represents your creditworthiness, with a higher score indicating better credit health.

On the other hand, a CIBIL report is a detailed document that contains your entire credit history, including loan accounts, credit card usage, repayment records, and past inquiries.

In short, the CIBIL score and report together provide lenders with a complete picture of your financial behavior before approving any credit.